In this article, we explore how debt financing is influencing UK mid‑market M&A. We elaborate on why understanding the current lending landscape has become essential for owner‑managed businesses considering a transaction. Debt financing involves using borrowed funds to support an acquisition, with repayments made from the future cash flows of the business rather than through dilution of ownership.

The landscape has shifted in recent years. Securing the right debt is now as much about preparation, structure and lender alignment as it is about cost. We outline the key trends shaping today’s market and highlight the practical considerations business owners should keep in mind as they plan their next steps.

Debt is no longer just about price in the UK mid-market, it’s about certainty, speed and structure. For owner-managed businesses, understanding the new dynamics can mean the difference between a deal that gets done and one that doesn’t.

UK mid‑market M&A: from 2025 slowdown to 2026 recovery

2025 was a year of recalibration. Elevated financing costs, the Capital Gains Tax (CGT) and National Insurance Contribution (NIC) increases from the Autumn Budget 2024 and persistent inflation all weighed on UK mid-market deal activity.

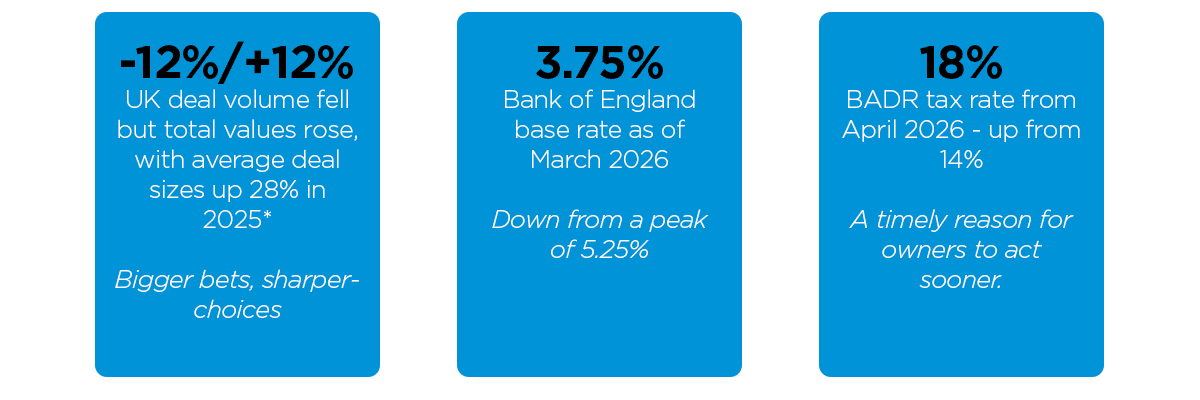

Volumes fell by around 12% in 2025. But the headline masks something interesting in deal dynamics. Total deal values rose 12% over the same period, when buyers transacted, they committed with conviction. The market didn’t necessarily slow down but instead became more selective.

2026 looks more encouraging. The Bank of England has cut its base rate from a peak of 5.25% to 3.75%, confidence is returning, with more sales coming to market. The doors aren’t thrown wide open, but they’re opening, for the right businesses.

The rise of private credit in UK mid‑market acquisitions

The most significant structural shift in acquisition finance has been the rise of private credit. Non-bank lenders, such as specialist debt funds, direct lending platforms and challenger banks, now dominate mid-market leveraged finance, with around 70% of private credit transactions carried out to support M&A activity. The competition among lenders is no longer just about price; it’s about flexibility, structure and speed of execution.

Crucially, these lenders are often willing to back a business on the basis of its recurring revenues and management quality. Rather than purely its tangible assets, making deals viable that traditional banks would decline.

Unitranche structures are now widely used. They combine what was once separate senior and junior loans into a single, blended facility, making deals simpler and more certain to execute. There is genuine capital looking for a home, and increasingly it is finding its way into the mid-market.

Why cash flow and financial covenants matter more than ever

Better access to debt doesn’t mean less scrutiny, quite the opposite. It is no longer enough to show healthy EBITDA, lenders want to understand how reliably that profit converts into actual cash. Cash conversion, working capital discipline and earnings quality are all under the microscope. EBITDA adjustments are examined closely, exceptional items are capped tightly, and downside scenarios are stress-tested more aggressively than they were even two years ago.

Financial covenants such as leverage tests and debt service cover ratios are back as standard after the covenant-lite era. For owner-managed businesses, the practical implication is clear. Well-presented financials, clearly articulated earnings and demonstrable cash generation are now deal-critical. Preparation isn’t the boring bit before the deal. It’s half the deal.

Which sectors attract the most acquisition financing?

Lender appetite varies significantly by sector. Technology-enabled services, healthcare, professional services and specialist business services attract strong interest and competitive terms, as businesses with resilient, recurring revenues are in high demand. This makes cybersecurity and AI-adjacent businesses particularly sought after. Highly cyclical or consumer-sensitive businesses, meanwhile, may find debt harder or more expensive to secure. Sector positioning, and the ability to articulate a credible, resilient investment case, has become a meaningful part of achieving the right financing on the right terms.

Deal structures bridging valuation gaps in UK M&A

Earn-outs, deferred consideration and vendor loan notes are all more prevalent than they were, helping bridge valuation gaps where upfront leverage is constrained. Buy-and-build strategies continue to dominate private equity activity, and for businesses being acquired as part of a consolidation platform, understanding the pre-agreed debt facility shaping that process is important context for any seller.

What this means for owner‑managed businesses considering a sale

Business Asset Disposal Relief (BADR) now attracts a tax rate of 18% (up from 14%), a meaningful difference in net proceeds for many owners. A timely prompt to consider strategic options. The debt markets are more navigable than they were twelve months ago. But they reward preparation: knowing which lenders are active, how to structure the deal and how to present your business in its best light.

At PEM we support owner‑managed businesses across Cambridge and beyond through all stages of the transaction lifecycle. Our approach combines practical insight with hands-on transactional experience.

If you’re considering a sale, acquisition or strategic investment, and would like to understand how debt financing could impact your transaction, we’d welcome a confidential conversation.

*Source: PwC